The Deflated Sharpe Ratio: Why a 2.5 Sharpe Can Still Be Statistical Noise

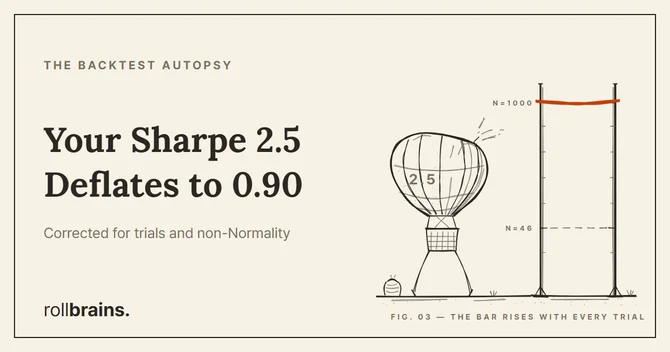

💡 Key Takeaways A high Sharpe is not evidence on its own. The Deflated Sharpe Ratio (DSR) corrects a backtest Sharpe for two inflation sources at once: selection bias from trying many strategies, and non-Normal (skewed, fat-tailed) returns. The bar moves with the number of trials. Even if the true Sharpe is zero, the expected maximum Sharpe across N independent trials is positive. DSR sets the rejection threshold to that expected maximum — so the more you search, the higher you must clear. The worked number is sobering. A Sharpe of 2.5 (5 years daily, skew −3, kurtosis 10) found after N=1000 trials has a DSR of only ≈ 0.90 — it fails the 95% bar. The identical result found after just N=46 trials would have passed at 0.9505. This explainer reconstructs the Deflated Sharpe Ratio strictly from the primary source — Bailey & López de Prado, “The Deflated Sharpe Ratio: Correcting for Selection Bias, Backtest Overfitting and Non-Normality” (Journal of Portfolio Management, 2014). It pairs with our empirical Backtest Autopsy series, which measures the failures this metric is designed to catch. ...